OxCARRE associate

Rabah Arezki and colleagues

Adnan Mazarei, and

Ananthakrishnan Prasad from the IMF, and also available on the IMFDirect blog

here, write on

Sovereign Wealth Funds in the New Era of Oil

By Rabah Arezki, Adnan Mazarei, and Ananthakrishnan Prasad

As

a result of the oil price plunge, the major oil-exporting countries are facing

budget deficits for the first time in years. The growth in the assets of their

sovereign wealth funds, which were rising at a rapid rate until recently, is

now slowing; some have started drawing on their buffers.

In

the short run, this phenomenon is not cause for alarm. Most oil exporters have

enough buffers to withstand a temporary drop in oil prices. But what will

happen if low oil prices persist, and how will policymakers react?

We explore here the fallout from low oil prices on sovereign

wealth funds in oil-exporting countries and find that that they have important

domestic implications. The impact on global asset prices will depend on the

extent to which the unwinding of oil exporters’ sovereign wealth funds is not compensated by portfolio

adjustment in other parts of the world.

The rise of sovereign wealth funds

The rise of sovereign wealth funds

In

the early 2000s, high oil prices brought about a massive redistribution of

income to oil exporters, resulting in

current account surpluses and a rapid buildup of foreign assets. Governments

established new sovereign wealth funds or increased the size of existing ones

to help manage the larger pool of financial assets.

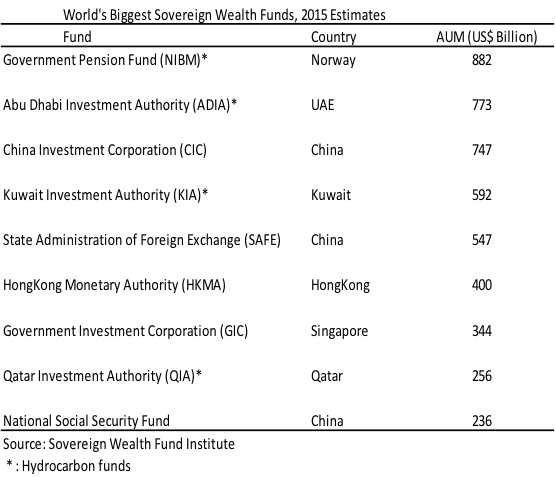

The total assets of sovereign wealth

funds are concentrated in a few countries. As of March 2015, it is estimated

at $7.3 trillion, of which $4.2 trillion are oil and gas related. While there

are large differences across sovereign wealth funds, available information on

their asset allocation points to a significant share in equities and

bonds.

Oil

prices and the redistribution of global income

With high oil prices

throughout the 2000s, the aggregate current account balance of exporters

reached about $630 billion in 2011, exceeding that of emerging Asia combined. The

current account surpluses of oil exporters are vanishing in 2015, however, and

it is unlikely that this decline will reverse soon. On current projections,

their combined current account balances could recover to about $200 billion in

2020.

With high oil prices

throughout the 2000s, the aggregate current account balance of exporters

reached about $630 billion in 2011, exceeding that of emerging Asia combined. The

current account surpluses of oil exporters are vanishing in 2015, however, and

it is unlikely that this decline will reverse soon. On current projections,

their combined current account balances could recover to about $200 billion in

2020.

In

contrast to the 2000s, the recent oil price drop has been driven mainly by

supply factors that may

lead to a decoupling of the paths of asset accumulation between these two

groups of sovereign wealth funds. The rate of asset accumulation by sovereign

wealth funds in emerging Asia—mostly oil importers—is likely to rise but it

will likely decline for the funds in oil-exporting countries. Of course, much

will depend upon the strategic asset allocation choices made by the largest sovereign

wealth funds in the low oil price environment.

Impact on global asset

markets

The

overall impact

of the fall in oil prices on asset prices will

depend on whether oil importers have a lower marginal propensity to save than

oil exporters. The fall in oil prices tends to transfer wealth from oil

exporters to high-saving emerging Asian countries—but also to many other

countries, including large advanced economies, some of which have a low

propensity to save. From a global perspective, this implies lower global saving

and higher interest rates.

Precisely

how much the savings of the sovereign funds of oil producers decline depends,

of course, on changes in their fiscal and external current account balances. Sovereign

wealth funds’ market operations will also depend on how much their governments opt

to borrow or draw on their fiscal buffers, including those kept with sovereign wealth

funds. Saudi Arabia issued its first sovereign bonds since 2007 to local banks

to finance its fiscal deficit.

In

addition, oil-exporters’ sovereign wealth funds are significant holders of U.S. treasury

debt and private equity. Our back-of-the-envelope calculations

show that, prior to the oil price decline, countries of the Gulf Cooperation

Council (GCC) alone were projected to have a combined fiscal surplus of about

$100 billion in 2015 and of about $200 billion between 2015 and 2020, but are

now likely to reach a combined deficit of $145 billion in 2015 and over $750

billion in 2015-20. This implies change in net assets available to sovereign

wealth funds in the GCC alone of $250 billion in 2015 and $950 billion in

2015-20.

Considering

the expected tightening in U.S. monetary policy—especially against the

background of concerns about market liquidity, increasing risk aversion, and falling

reserve holdings by some emerging markets—a substantial change in the path of

asset accumulation by sovereign wealth funds will likely have a direct effect

on financial markets.

A

study by economists at

the Federal Reserve has shown that if foreign official inflows into

U.S. Treasuries were to decrease in a given month by $100 billion, five-year

Treasury rates would rise by about 40 to 60 basis points in the short-run, with

a long-run effect of about 20 basis points.

Domestic implications

What does all this mean for the accumulation of

sovereign wealth in oil-exporting countries, at least in the medium term?

The

low price environment is likely to test the relationship between governments in oil-exporting countries and their sovereign wealth funds. Absent

cuts in public expenditures, governments will likely be transferring less

revenue than before to these funds. At the same time, pressures to draw down on

sovereign wealth funds’ assets will probably rise.

Among Middle East oil exporters, only the United

Arab Emirates, Qatar, and Kuwait’s fiscal buffers will last for over 25 years

on current fiscal plans and oil price projections, according to our estimates.

Bahrain and Yemen will exhaust them in the next two years, while most other

countries will run out of buffers in four to seven years.

Even though they’ll still be able to borrow

to finance their spending, governments of these oil-exporting countries would

probably do well to tighten their belts if they hope to achieve the dual

objective of sharing oil wealth equitably with future generations and economic

stabilization.